What Is A Sinking Fund? The Simple Savings Strategy That Changed How I Budget

I remember the exact moment I realized I was doing money wrong.

It was a scorching summer day in Florida. The kind of day where the humidity hits you like a wall the second you step outside. I was driving home from work at the dealership, and my car’s AC just stopped blowing cold. No warning. No gradual decline. Just hot air.

I was lucky enough to work at a dealership, so I got it looked at the next day. As it turns out, I needed a new radiator. The bill? $500 for parts plus labor. I paid nearly $900 to get my AC blowing cold again.

That $900 came straight from my checking account. It wiped out what I had been saving for other things. And the worst part? Car repairs are not exactly a surprise. Cars break down. It happens. I just never planned for it.

That is when I discovered sinking funds. And honestly, it changed everything about how I budget.

A sinking fund is a savings strategy where you set aside small amounts of money over time for a specific, planned expense. Instead of getting blindsided by high costs, you prepare for them in advance. It is one of the simplest, most effective ways to take control of your personal finances and stop living paycheck to paycheck.

In this guide, I will walk you through exactly what a sinking fund is, how it works, why it is different from an emergency fund, and how to set one up today. Whether you are new to budgeting or looking for a better way to handle big expenses, this strategy is for you.

What Is a Sinking Fund?

A sinking fund is a dedicated savings account (or portion of your budget) where you save small, regular amounts of money toward a specific future expense. The idea is simple: instead of scrambling to pay for something big all at once, you break it into smaller, manageable contributions over weeks or months.

Think of it like this. You know Christmas is coming every December. You know your car insurance is due every six months. You know your pet needs a vet visit once a year. These are not surprises. They are predictable expenses. A sinking fund lets you prepare for them ahead of time.

According to NerdWallet, a sinking fund is built up over time with regular deposits and helps you pay for big costs without relying on credit cards or draining your emergency fund.

The term “sinking fund” originally comes from the business and government world, where organizations would set aside money gradually to pay off a future debt. In personal finance, the concept works the same way. You are “sinking” a little money away each month so that when the expense arrives, you are ready.

Here is a quick example. Let is say your car insurance costs $600 every six months. Instead of scrambling to find $600 in one month, you save $100 per month for six months. When the bill arrives, the money is already there. No stress. No credit card debt. No pulling from your emergency fund. That is the power of a sinking fund.

How Sinking Funds Work

The mechanics of a sinking fund are straightforward. Here is how it works in four simple steps.

Step 1: Identify a specific expense you know is coming. This could be anything from a vacation to new tires to holiday gifts.

Step 2: Determine the total cost. Research or estimate how much you will need. It does not have to be exact, but get close.

Step 3: Set a deadline. When do you need the money? Three months from now? Six months? A year?

Step 4: Divide the total by the number of months until your deadline. That is your monthly contribution.

Here is a real example. Let us say you want to save $1,200 for a family vacation in 12 months. You divide $1,200 by 12 months, and you get $100 per month. Set up an automatic transfer of $100 on payday, and by the time your trip rolls around, the money is sitting there waiting for you.

The key difference between a sinking fund and just “saving money” is the specificity. Every dollar in a sinking fund has a name. It has a purpose. It has a deadline. That clarity is what makes it so effective.

You can have multiple sinking funds running at the same time. One for car maintenance, one for Christmas gifts, one for your annual insurance premium. Each one gets its own balance and its own monthly contribution.

Sinking Fund vs. Emergency Fund: What Is the Difference?

This is one of the most common questions I get, and it is a great one. A sinking fund and an emergency fund are both savings tools, but they serve very different purposes.

An emergency fund is money set aside for truly unexpected, unplanned events. A job loss. A medical emergency. A major home repair you could not have predicted. The Consumer Financial Protection Bureau recommends building an emergency fund as a financial safety net for these kinds of shocks.

A sinking fund, on the other hand, is for planned, predictable expenses. You know they are coming. You just need to save for them in advance.

Here is a simple way to think about it:

Emergency fund: “I did not see that coming.” Covers job loss, medical bills, unexpected home repairs, and other true emergencies.

Sinking fund: “I knew this was coming.” Covers car maintenance, holidays, insurance premiums, vacations, and other planned expenses.

The biggest mistake I see people make is using their emergency fund for expenses that are not actually emergencies. Car maintenance is not an emergency. It is a fact of car ownership. Christmas is not an emergency. It comes every single year on December 25th.

When you use sinking funds for predictable expenses, your emergency fund stays intact for the real surprises. That is how you build a complete financial safety net.

Why Sinking Funds Changed How I Budget

Before I started using sinking funds, my budget felt like it was constantly under attack. Every few months, something “unexpected” would pop up: a car repair, an insurance bill, a birthday gift I forgot about. And each time, it threw my whole budget off track.

I was frustrated. I felt like I could never get ahead. No matter how carefully I tracked my spending, these big expenses kept wiping out my progress.

Then I sat down and made a list of every non-monthly expense I could think of. Car maintenance. Insurance premiums. Holiday gifts. Annual subscriptions. Vet bills. Home repairs. It was a long list.

And here is what hit me: none of these were actually unexpected. I knew my car needed oil changes and tire rotations. I knew Christmas was coming. I knew my insurance was due every six months. The only reason they felt like emergencies was because I never planned for them.

That is when I set up my first sinking funds. I started small. Just three: one for car maintenance, one for Christmas gifts, and one for my car insurance premium.

Within a few months, something shifted. When my car needed new brakes, the money was already there. When December rolled around, I had gift money ready to go. When my insurance bill arrived, I paid it without even thinking about it.

The stress just disappeared. My budget finally felt stable. I stopped living in a cycle of financial whiplash, and I started actually making progress toward my bigger goals.

If you are tired of feeling like your budget is broken every time a big expense pops up, sinking funds are the fix. I am living proof.

Common Sinking Fund Categories

One of the best things about sinking funds is that you can create one for just about any planned expense. Here are some of the most popular categories to get you started.

Home and Living: rent deposit, home repairs, furniture, appliances, property taxes, HOA fees.

Transportation: car maintenance, car insurance, new tires, registration and tags, next car down payment.

Health and Medical: annual physicals, dental cleanings, vision exams, prescriptions, health insurance deductible.

Holidays and Gifts: Christmas, birthdays, anniversaries, Mother’s Day, Father’s Day, Valentine’s Day.

Personal and Lifestyle: vacations, clothing, electronics, haircuts, self-care, subscriptions.

Education and Career: tuition, textbooks, certifications, professional development, work wardrobe.

Pets: vet visits, grooming, medications, pet insurance deductible.

I have a full breakdown of 20 sinking fund categories with real dollar examples in my post on sinking fund categories. If you want to see exactly how to budget for each one, check that out next.

The key is to start with the categories that cause you the most financial stress. For me, that was car maintenance and holiday gifts. For you, it might be something completely different. There is no wrong answer.

How to Set Up Your First Sinking Fund (Step-by-Step)

Setting up a sinking fund takes about 15 minutes. Here is exactly how to do it.

Step 1: List Your Predictable Expenses

Grab a piece of paper or open a note on your phone. Write down every non-monthly expense you can think of. Do not worry about the amounts yet. Just get them all on paper.

Think about what caught you off guard last year. Was it a car repair? A holiday gift? A medical bill? Those are your top sinking fund candidates.

Step 2: Estimate the Cost of Each Expense

Next to each expense, write down how much you think it will cost. Use last year as a reference if you have it. If not, do a quick search or estimate on the high side.

For example: Car maintenance, $1,200 per year. Christmas gifts, $500. Car insurance, $600 every six months.

Step 3: Set Your Timeline

Decide when each expense is due. Some are annual (like insurance). Some are seasonal (like holiday gifts). Some are ongoing (like car maintenance).

Step 4: Calculate Your Monthly Contribution

Divide the total cost by the number of months until the expense is due. That is your monthly sinking fund contribution.

Example: $1,200 for car maintenance divided by 12 months = $100 per month.

Step 5: Open a Separate Savings Account (or Use Sub-Accounts)

I recommend keeping your sinking fund money separate from your regular checking account. This makes it harder to accidentally spend it.

Many online banks let you create multiple savings sub-accounts. This is perfect for sinking funds because you can label each one: “Car Maintenance,” “Christmas,” “Vacation,” etc.

Step 6: Automate Your Transfers

Set up automatic transfers from your checking account to your sinking fund accounts on payday. When it is automatic, you do not have to think about it. The money moves before you even see it.

This is the most important step. Automation removes the temptation to skip a month or spend the money on something else.

How Much Should You Save in a Sinking Fund?

The amount you save in each sinking fund depends on three things: the total cost of the expense, when you need the money, and what you can realistically afford each month.

Here is the simple formula:

Monthly contribution = Total expense divided by number of months until due.

Let me give you a few real examples.

Vacation: $2,400 trip in 12 months = $200 per month.

Car insurance: $600 due in 6 months = $100 per month.

Christmas gifts: $600 in 10 months = $60 per month.

New laptop: $1,000 in 8 months = $125 per month.

If those numbers feel too high, you have two options. You can extend your timeline (save for 18 months instead of 12). Or you can reduce the total amount (plan a $1,500 vacation instead of $2,400).

The point is not to save exactly the right amount. The point is to save something consistently. Even $25 per month toward car maintenance is better than nothing.

Start where you are. Use what you have. Do what you can. You can always increase your contributions later as your income grows or as you pay off other debts.

Best Ways to Track Your Sinking Funds

Once you have your sinking funds set up, you need a system to track them. Here are the most popular methods.

Envelope Method:

If you prefer cash budgeting, you can use physical envelopes for each sinking fund. Label each envelope and add cash on payday. This method works great for people who are visual and hands-on with their money. I wrote a full guide on the envelope budgeting system if you want to learn more.

Spreadsheet:

A simple spreadsheet works well if you like seeing all your numbers in one place. Create a column for each sinking fund, track your monthly contributions, and watch the balances grow.

Banking Sub-Accounts:

Many online banks (like Ally, Capital One 360, or SoFi) let you create multiple savings buckets. This is my personal favorite method because the money is separated and labeled right inside your bank.

Budgeting Apps:

Apps like YNAB (You Need A Budget), Monarch Money, or EveryDollar have built-in features for tracking sinking funds. If you already use a budgeting app, this is the easiest way to get started.

Common Sinking Fund Mistakes to Avoid

Sinking funds are simple, but there are a few common mistakes that can trip you up. Here is what to watch out for.

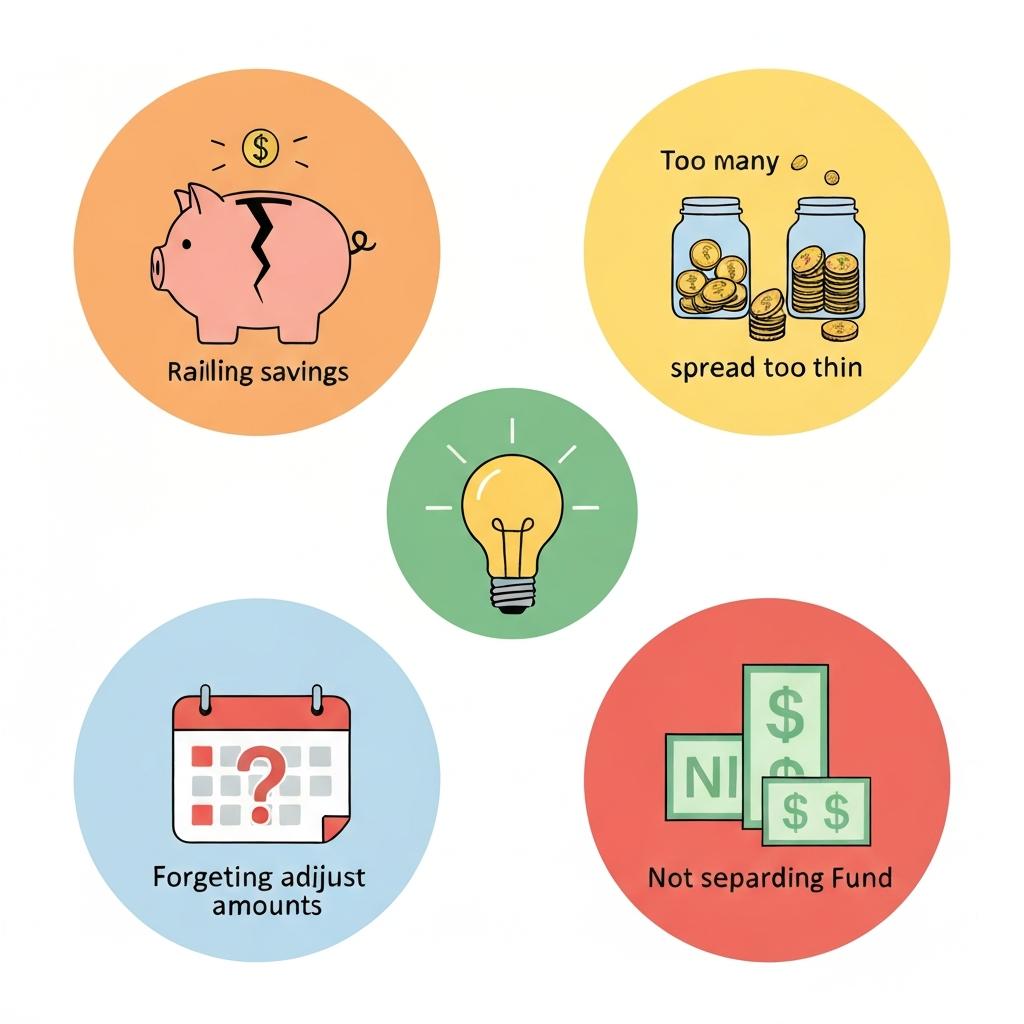

Mistake 1: Not Starting Because the Amount Feels Too Small

I hear this all the time. “I can only save $20 a month, so what is the point?” The point is that $20 per month becomes $240 in a year. That is $240 more than you would have had. Small amounts add up. Start with whatever you can afford, even if it feels insignificant.

Mistake 2: Raiding Your Sinking Fund for Other Expenses

Your car maintenance fund is for car maintenance. Not for pizza. Not for a new pair of shoes. When you start borrowing from one fund to cover another, the whole system falls apart. Treat each sinking fund as untouchable for anything other than its intended purpose.

Mistake 3: Having Too Many Sinking Funds at Once

When you first discover sinking funds, it is tempting to create one for everything. But spreading your money across 15 different funds means each one grows very slowly. Start with 3 to 5 funds for your highest-priority expenses. You can always add more later.

Mistake 4: Forgetting to Adjust Your Amounts

Life changes. Prices go up. Your income might change. Review your sinking fund amounts every few months and adjust as needed. If car insurance went up by $50, update your monthly contribution. If you got a raise, put some of that extra money toward your funds.

Mistake 5: Keeping Sinking Fund Money in Your Checking Account

If your sinking fund money sits in the same account as your spending money, you will spend it. Move it to a separate savings account where it is out of sight and out of mind. The small friction of having to transfer money back is often enough to stop impulse spending.

Start With Just One

If you are reading this and feeling overwhelmed by all the sinking fund categories and numbers, take a deep breath. You do not need to set up 10 funds today.

Start with just one.

Pick the expense that stresses you out the most. Maybe it is car repairs, like it was for me. Maybe it is holiday gifts or your insurance premium. Whatever it is, set up one sinking fund, automate one small transfer, and watch what happens.

Within a few months, you will feel the difference. That weight on your shoulders will get a little lighter. And you will wonder why you did not start sooner.

I know because that is exactly what happened to me. That $900 AC repair taught me a painful lesson. But sinking funds made sure I never had to learn it again.

You got this! Start with just one today.

Disclaimer: This post is for educational purposes only and does not constitute financial advice. Please consult a qualified financial professional for advice specific to your situation.

Frequently Asked Questions

What is a sinking fund in simple terms?

A sinking fund is money you save a little at a time for a specific expense you know is coming. Instead of paying a big bill all at once, you break it into smaller monthly savings so the money is ready when you need it.

How many sinking funds should I have?

Start with 3 to 5 sinking funds for your highest-priority expenses. Once those are established and funded, you can add more. Too many at once spreads your money thin and makes it hard to see progress.

Where should I keep my sinking fund money?

The best place is a high-yield savings account at an online bank. Many online banks let you create multiple sub-accounts or “buckets” so you can label each sinking fund separately. This keeps the money earning interest while staying organized.

How is a sinking fund different from an emergency fund?

An emergency fund covers truly unexpected events like job loss or medical emergencies. A sinking fund covers planned, predictable expenses like car maintenance, insurance premiums, and holiday gifts. You need both for a complete financial safety net.

How often should I contribute to my sinking funds?

Contribute on every payday. If you get paid biweekly, make a transfer every two weeks. If you get paid monthly, transfer once a month. The key is consistency. Automating your transfers makes this effortless.