How To Create A Budget That Actually Works | A Simple Guide

Did you know that 59% of Americans don’t track their spending at all? Crazy, right?! It’s no wonder budgeting feels overwhelming for many people. I used to be the same way: money in, money out, and no idea where it was going.

Creating a budget literally changed everything for me. It’s not about restricting yourself; it’s about giving every dollar a purpose so you stay in control instead of feeling stressed.

In this guide, I’ll walk you through exactly how to create a budget that actually works. Whether you’re living paycheck to paycheck or simply trying to save more for the future, these steps will help you establish a system that’s simple, realistic, and built to last.

What Is a Budget and Why Do You Need One?

When I first heard the word “budget,” I thought of restrictions, spreadsheets, and no fun money. Honestly, I pictured myself eating ramen noodles for the rest of my life so that I could save a few bucks. But that’s not what a budget is. At its core, a budget is simply a plan for your money, a way to tell your cash where to go instead of wondering where it went.

Think of it like a GPS.

You wouldn’t jump in the car for a road trip without directions, right? Well, money works the same way. If you don’t guide it, it’ll drift, usually toward takeout, subscriptions you forgot to cancel, or late-night Amazon splurges (been there 🙄).

One of the biggest myths I had to unlearn was that “budgets are only for broke people.”

Wrong!!

Wealthy people budget too; they call it a spending plan.

Another myth? “Budgeting means I’ll never get to have fun.” Again, nope. A good budget includes fun money. The difference is that you actually plan for it.

Why does this matter so much in 2025 and beyond?

Because inflation is still eating away at our paychecks, housing is expensive, and the cost of groceries feels like highway robbery.

Without a plan, your money evaporates.

But with a budget, you gain clarity, peace of mind, and actual savings.

For me, the biggest benefit wasn’t even financial; it was emotional. I slept better knowing my bills were covered and that I was making progress toward my goals.

Bottom line: A budget isn’t about restriction, it’s about freedom. Freedom from paycheck-to-paycheck stress. Freedom to save for the things that matter. And freedom to actually enjoy your money guilt-free.

Steps to Create a Budget That Works

When I made my very first budget, I overcomplicated it with too many categories. It failed within a month. So trust me when I say: keep it simple at first. Here’s the process I eventually landed on that stuck:

Step 1: Track your income

List every source, your paycheck, side hustles, even rental income. Write down your total take-home pay, not just gross income.

Step 2: List your expenses

Start with your fixed bills, such as rent/mortgage, utilities, and insurance. Then add variable expenses, such as groceries, gas, eating out, and subscriptions.

Step 3: Categorize your spending

Break it into “needs” (housing, food, bills) and “wants” (entertainment, travel, shopping). This helps you see where your money leaks.

Step 4: Choose a budgeting method

If you’re brand new, try the 50/30/20 budgeting rule: 50% needs, 30% wants, 20% savings. If you want tighter control, the zero-based budget works better.

Step 5: Set financial goals

Maybe it’s saving $1,000 for an emergency fund, paying off your credit card, or stashing cash for a trip. Having a target keeps you motivated.

Step 6: Adjust monthly

Budgets aren’t set in stone. Every month, check what worked and what didn’t. Overspent on food? Adjust. Got a raise? Redirect extra income.

The key is flexibility. Your first budget won’t be perfect, and that’s okay. Mine definitely wasn’t. But with tweaks, it became second nature, and that’s when the real progress started.

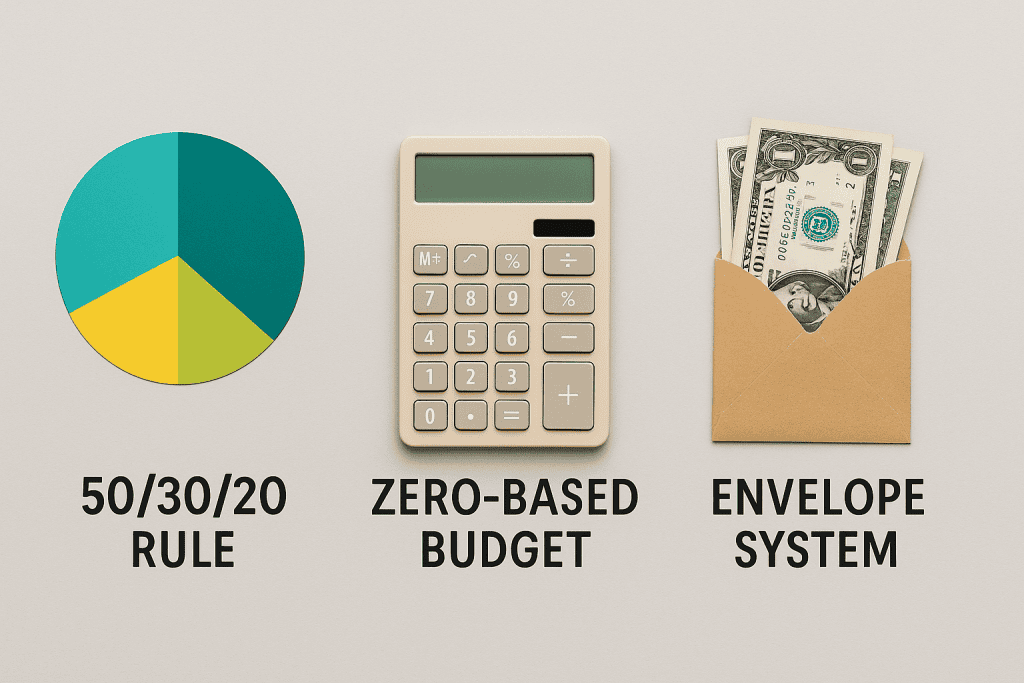

Popular Budgeting Methods Explained

There isn’t a one-size-fits-all budget. The trick is finding one that fits your personality and lifestyle.

Let me break down the most popular ones I’ve tried:

50/30/20 Rule

This one’s great for beginners. Super simple: 50% to needs, 30% to wants, 20% to savings/debt.

If you don’t want to track every latte, this works.

Zero-Based Budget

My personal favorite was when I was paying off debt. You assign every single dollar a “job” until your income minus expenses equals zero. It forces you to be intentional.

Envelope/Cash System

Ah, the envelope budgeting system. This saved me back when I couldn’t stop overspending on groceries and eating out. You literally put cash in envelopes (or use digital versions) and stop when it’s gone. Old-school, but it works.

Digital Budgeting Tools

If you hate manual tracking, apps like YNAB, GoodBudget, or Rocket Money automate most of it. I used Google Sheets at first, then upgraded to an app when things got messy.

My advice? Try one method for at least 2 to 3 months. If it doesn’t click, switch. Budgeting is like fitness; you’ve got to find the workout you’ll actually stick to.

Tools and Apps to Help You Budget

When I first started budgeting, I used a notebook and a pen. Simple, but wow, it was a pain keeping track of every little thing.

Eventually, I moved to Google Sheets, and that was a game-changer. But when life got busier, I realized I needed apps that could automate the process. If you’re anything like me, the right tools can mean the difference between a budget that fails in two weeks and one that sticks for years.

Here are a few I’ve personally tried or seen others swear by:

1. Free Budgeting Apps. If you’re new to budgeting and don’t want to spend money, start with something like Goodbudget. It uses the envelope budgeting system and is easy to use. Fill in your transactions, and it gives you a quick overview of where your money’s going.

2. Paid Options. After a while, I graduated to YNAB (You Need a Budget). This app completely shifted how I thought about money. It uses the zero-based budget method and forces you to “give every dollar a job.” It’s not free, but I found it worth the subscription because it made me stick to my goals. Another good paid option is EveryDollar, which was built around the Dave Ramsey budgeting style.

3. Spreadsheet Lovers. If you like control (and don’t mind a little nerding out), Google Sheets or Excel can be super powerful. You can build a custom budget template, color-code categories, and even create charts. I actually enjoyed tinkering with mine, though sometimes I spent more time making the spreadsheet look pretty than tracking my spending (oops 😅).

4. Hybrid Tools. Recently, apps like Rocket Money have grown in popularity. They don’t just track spending, they also cancel subscriptions you forgot about, track bills, and help you negotiate lower rates. Honestly, this one saved me money on my internet bill without me having to make a single phone call.

5. Credit & Savings Apps. If you’re pairing budgeting with savings goals, consider using apps like Acorns (which rounds up your purchases to invest) or Chime (which offers automatic savings features). These aren’t pure budgeting apps, but they help you build better money habits.

The truth is, the “best” tool depends on your personality.

Do you want hands-off automation? Go with YNAB or Rocket Money.

Do you want detailed control? YNAB or spreadsheets will be your friend. The key is finding something you’ll actually use, because a tool only works if you stick with it.

When I finally got serious about budgeting, YNAB was the one that kept me consistent. But I still recommend starting free before paying for anything. That way, you’ll know what features you actually need instead of just chasing fancy dashboards.

Budgeting Tips to Stay Consistent

I’ll be real with you, starting a budget is easy, but sticking with it is the hard part. The first time I made a budget, I was pumped. I had my categories, notebook, and pen ready to get started!

Two weeks in? I gave up because I overspent on takeout and felt like a failure. If that’s happened to you too, don’t worry, it’s normal. Staying consistent takes a little strategy, and these are the tricks that finally worked for me.

Start simple. Don’t make the mistake I did and create 30 categories. You’ll get burned out. Instead, lump things together: housing, food, transportation, debt, savings, fun. You can always get more detailed later once you’ve built the habit.

Automate whenever possible. Bills, savings, debt payments – set them to auto-pay. When I finally automated my savings, I noticed it actually grew because I wasn’t tempted to “skip it this month.” Out of sight, out of mind, works wonders here.

Use sinking funds. This one was a game-changer for me. Instead of getting slammed by Christmas shopping or car repairs, I started setting aside small amounts every month. For example, I put $100/month into a “car repairs” fund. Six months later, when I needed new brakes, the money was already there. No panic.

Build in fun money. This is the biggest secret to not hating your budget. Seriously, don’t try to cut out every little joy. I budget $200/month for fun, and I can spend it guilt-free. The key is balance; if you feel deprived, you’ll give up.

Track weekly, not monthly. Waiting until the end of the month is too late. I started doing a quick 10-minute check-in every Sunday. Open the app, see where you stand, and make small adjustments. It keeps you from being blindsided later.

Have accountability. If you’re married or living with someone, do the budget together. If you’re single, tell a friend about your goals. When I first started, I actually had a buddy I’d text once a week with my savings progress. Knowing someone else was watching helped me stay on track.

Consistency is really about momentum. The first month will be messy. The second month was a little smoother. By month three, you’ll feel like you’re finally getting the hang of it. And remember, a “bad” budgeting month doesn’t mean failure, it just means you’ve got real data to improve on next time.

The truth? Budgets are like diets.

If it’s too strict, you’ll break it. If it’s realistic and flexible, you’ll stick with it for years. And sticking with it is where the magic happens, savings pile up, debt melts away, and suddenly you’re in control instead of money controlling you.

Common Budgeting Mistakes to Avoid

When I think back to my very first budget, I honestly laugh. I was so proud of myself, but I made almost every mistake possible. It wasn’t that budgeting didn’t work; it was that I set myself up to fail without realizing it. If you’re just starting out, here are the biggest traps I’ve fallen into (and seen others fall into) that you’ll want to dodge.

Forgetting irregular expenses. This was my number one mistake. I’d plan for rent, groceries, gas, and the basics. But then Christmas rolled around, or my car needed new tires, and bam! I’d swipe my credit card and feel like my budget was useless. The fix? Sinking funds. Even $20/month toward “future expenses” adds up fast and saves you from those “oh no” moments.

Not updating your budget. A budget isn’t a one-and-done thing. My first budget looked perfect on paper, but I didn’t adjust when gas prices went up or when I got a small raise. By month two, it was outdated and useless. I’ve learned to tweak it monthly, like a living document.

Being too strict. In my early budgeting days, I cut out everything fun. No coffee shops, no movies, no takeout. Guess how long that lasted? About two weeks. A budget without joy is like a diet with no cheat meals; it won’t stick. Now, I plan for fun spending so I don’t feel guilty.

Focusing only on cutting costs. Yes, saving matters. But I made the mistake of only looking for things to cut, instead of thinking about how to increase my income. Side hustles, freelancing, even selling stuff I didn’t use, all of that gave me breathing room in my budget that I couldn’t have achieved just by cutting Netflix.

Not tracking small purchases. Oh man, the $5 here and $10 there adds up fast. For months, I wondered why I was “failing” at budgeting, only to realize it was daily snacks, random apps, and those sneaky Amazon “add-ons.” I finally started logging every purchase (apps make this way easier), and the leaks were obvious.

Quitting after a bad month. This is the mistake that almost had me giving up for good. I’d blow the food budget one month and think, “Well, I suck at this.” But that’s not how it works. Budgets are meant to be flexible and improved over time. Now I see overspending as data, not failure.

The truth? A budget is like training wheels for your money. You’re going to wobble. You might even crash. But if you learn from each mistake and keep going, you’ll eventually ride smoothly. I promise, the people who succeed at budgeting aren’t perfect; they’re just the ones who didn’t quit.

Example of a Simple Monthly Budget

One of the things that held me back from budgeting for so long was that I couldn’t picture what a “real” budget looked like.

I read tons of articles, but they all gave me vague advice like “spend less than you earn” (gee, thanks!). What finally clicked for me was seeing an actual breakdown with real numbers. So let’s walk through an example together.

Let’s say you bring home $3,000 a month after taxes. Here’s a super simple way you might split it up using the 50/30/20 rule:

Needs (50% = $1,500)

- Rent/Mortgage: $900

- Utilities: $150

- Groceries: $300

- Transportation (gas, bus, etc.): $150

Wants (30% = $900)

- Eating out: $200

- Entertainment (Netflix, concerts, movies): $150

- Shopping: $200

- Travel fund: $350

Savings & Debt (20% = $600)

- Emergency fund: $200

- Retirement savings (401k, IRA): $200

- Debt payoff (credit card, student loan): $200

Boom! That’s a complete budget. Notice how it covers the essentials, gives you guilt-free fun money, and still pushes savings forward.

Now, if you’re more detail-oriented (like I was when I switched to a zero-based budget), you can break it down even further.

For example:

- Housing: 30%

- Food: 15%

- Transportation: 10%

- Savings: 15%

- Debt payoff: 10%

- Fun/Entertainment: 10%

- Miscellaneous/Irregular: 10%

One thing I recommend?

Always include a “miscellaneous” category. Life throws curveballs, whether it’s a birthday gift you forgot about or an extra school expense. Having a cushion for those prevents your budget from blowing up.

If you’re more of a visual learner, you can make this even easier with a spreadsheet or app. Personally, I like seeing pie charts of my money because it shows me where the bulk of it goes. Google Sheets and budgeting apps can generate those with just a little setup.

Here’s a quick budget template you can copy (works on paper, too):

- Write down your monthly income.

- Subtract fixed expenses (rent, utilities, insurance).

- Subtract variable expenses (groceries, gas, eating out).

- Assign a set % to savings/debt.

- Whatever’s left goes into wants/fun.

The beauty is you don’t need fancy tools to get started; you need clarity. Once you see your money on paper (or screen), it’s easier to make smarter choices. And trust me, nothing feels better than realizing you do have enough to cover your bills and still enjoy life.

Take Control of Your Money Today

Here’s the truth: budgeting isn’t about being perfect; it’s about being intentional. When I first started, I thought I had to track every single cent with military precision.

Spoiler alert: I failed, more than once. But over time, I realized that a budget is less about restriction and more about freedom. Freedom from stress, freedom from debt, and freedom to enjoy the things you love without guilt.

The hardest part is always starting. That first time you sit down and look at your income versus expenses can be uncomfortable.

You might even feel embarrassed about how much you’ve been overspending. I sure did. But here’s the thing: that moment of honesty is the first step toward financial control.

And once you’ve got that, you can build anything: an emergency fund, debt payoff, even early retirement if that’s your dream.

Remember, your budget doesn’t have to look like anyone else’s. Maybe you thrive with the 50/30/20 rule. Maybe you prefer zero-based budgeting. Or maybe you just want a simple spreadsheet and a little accountability. The method doesn’t matter nearly as much as the consistency.

So here’s my challenge to you: start today! Grab a notebook, download an app, or open a spreadsheet. Write down your income and expenses, then give every dollar a job.

Please keep it simple, give yourself room for fun, and stick with it for at least three months. By then, you’ll be amazed at how much progress you’ve made.

Future-you will thank you for the effort you put in now. Your savings will grow, your stress will shrink, and you’ll finally feel in control of your money instead of the other way around.

Ready to take control?

Go create your first budget today!

Frequently Asked Questions About Creating a Budget

What is the easiest way to start a budget?

The easiest way is to write down your income and list out your essential expenses (rent, groceries, bills). From there, choose a simple method like the 50/30/20 rule: 50% needs, 30% wants, 20% savings. Don’t overcomplicate it in the beginning.

How much should I save each month on a budget?

A good target is at least 20% of your income, but if that’s not realistic, start smaller. Even $50 or $100 a month adds up. The key is consistency; saving regularly matters more than the exact amount.

What are the most common budgeting mistakes?

The biggest mistakes include forgetting irregular expenses (such as holidays or car repairs), being too strict with no allowance for fun, and quitting after one bad month. Budgets are flexible; adjust, don’t abandon them.

Can I use apps to make budgeting easier?

Absolutely. Free apps like GoodBudget or paid ones like YNAB (You Need a Budget) can connect to your bank accounts and automatically track expenses. If you prefer full control, Google Sheets or Excel work great too.

How do I stick to a budget without feeling restricted?

The secret is to include fun money in your budget. Plan for entertainment, eating out, or hobbies so you don’t feel deprived. Budgets aren’t about saying “no” to everything—they’re about spending with intention.