50/30/20 Budgeting Rule: How To Use It To Manage Your Money Better

When I first tried budgeting, it felt like I needed a finance degree just to make sense of it.

Between budgeting apps, spreadsheets, and complicated rules about where every dollar should go, I’d always end up frustrated, and honestly, broke by the end of the month.

That’s when I discovered the 50/30/20 budgeting rule, a simple, no-stress way to manage money that actually made sense.

Instead of tracking every single transaction or giving up everything I loved, this rule gave me structure and flexibility. It showed me exactly how to spend, save, and enjoy my money without feeling guilty. I felt like I was finally able to battle my bad money habits!

In this post, I’ll walk you through how to use the 50/30/20 budgeting rule step-by-step, what it means, how to calculate your own budget, and how to make it work for your lifestyle.

By the end, you’ll know exactly how to take control of your money and finally feel good about your spending.

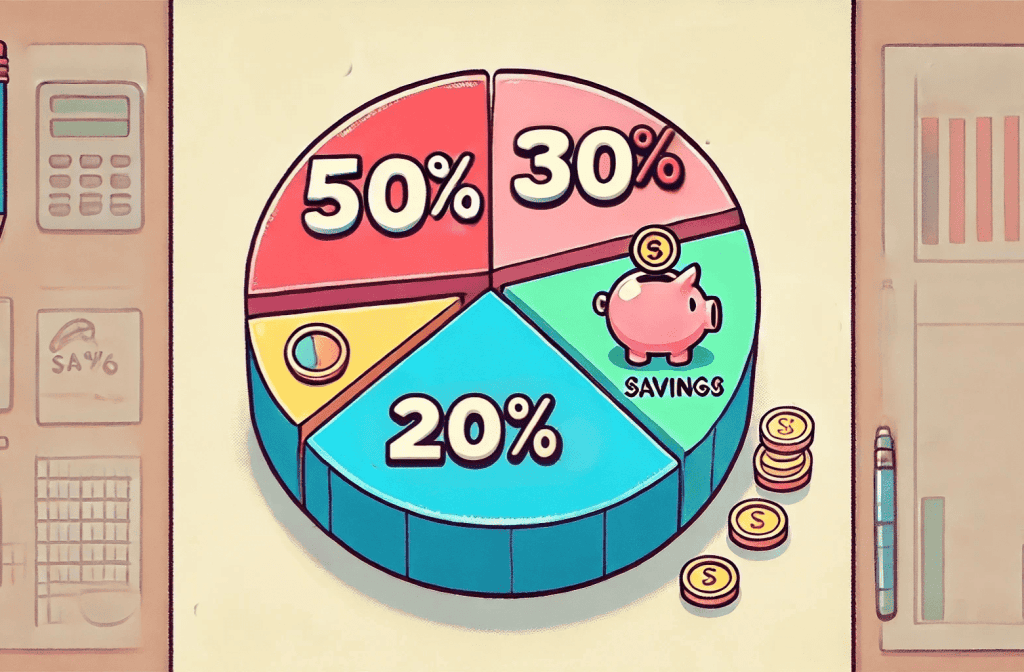

What Is The 50/30/20 Budgeting Rule?

If you’ve ever tried budgeting and felt completely lost, the 50/30/20 budgeting rule is like a breath of fresh air. It’s simple, practical, and works no matter how much you earn.

The idea is straightforward:

Divide your after-tax income into three main categories; Needs, Wants, and Savings/Debt.

It was popularized by U.S. Senator Elizabeth Warren in her book “All Your Worth: The Ultimate Lifetime Money Plan.” And while the concept’s been around for years, it’s still one of the easiest and most flexible ways to manage your finances.

Here’s the breakdown:

|

Category |

Percentage |

Purpose |

|---|---|---|

|

50% – Needs |

The essentials: rent, food, utilities, transportation, insurance |

Keeps your life running smoothly |

|

30% – Wants |

Fun stuff: dining out, entertainment, travel, shopping |

Adds joy and balance to life |

|

20% – Savings or Debt |

Savings, emergency fund, investments, debt repayment |

Builds financial security and freedom |

That’s it. No complex formulas, no endless tracking.

The 50/30/20 budgeting rule gives your money a clear structure while leaving room for flexibility, which is what most strict budgets fail to do.

If traditional budgeting feels too rigid, this method is the perfect middle ground. It keeps your spending under control without sucking the fun out of your life.

Breaking Down The 50/30/20 Budgeting Rule

50% – Needs

This is the foundation of your budget, the non-negotiables that keep your life running.

When I first tried this rule, I realized my “needs” list was… a little too long. Streaming subscriptions, fancy coffee, and weekend takeout all somehow made the cut. 😅

But here’s the truth: your needs are only the things you truly can’t live without; the essentials required to survive and work.

Here’s what belongs in this category:

- Rent or mortgage

- Utilities (electric, water, gas, internet)

- Groceries

- Transportation (gas, car payment, insurance, bus/train fare)

- Health insurance or medical costs

- Minimum debt payments

If these expenses take up more than 50% of your take-home pay, don’t panic, that’s super common, especially in high cost-of-living areas.

Here’s what you can do:

- Look for small ways to cut costs (like switching insurance plans or negotiating bills).

- Aim to gradually bring this category down to 50%, it doesn’t need to happen overnight.

Think of “needs” as your financial safety zone, keep it lean, but solid. It’s not about deprivation; it’s about stability.

30% – Wants

Here’s the part that makes this budgeting method feel realistic.

Because let’s be honest, we all need room for the things that make life fun.

When I first started budgeting, I tried to cut out every “non-essential” purchase… and it backfired fast. Within weeks, I was burnt out and ended up overspending even more.

That’s when I realized the 50/30/20 budgeting rule works because it includes space for fun.

Your “wants” are anything that’s not essential to your survival but adds joy or comfort to your life.

Think of things like:

- Eating out or grabbing coffee

- Streaming subscriptions

- Travel and entertainment

- Gym memberships

- Clothes and shopping

- Upgrades or hobbies

The key is to enjoy these things intentionally, not impulsively.

Try this simple mindset shift:

“Wants are rewards, not reactions.”

That means you plan for them, you look forward to them, but you don’t use them to cope with stress or boredom.

When your “wants” stay around 30%, you get to enjoy life and make steady financial progress. That’s the real sweet spot.

20% – Savings and Debt Repayment

This is the part of your budget that builds freedom.

When I first started following the 50/30/20 budgeting rule, this 20% category felt impossible. Between bills and daily expenses, I couldn’t imagine setting that much aside. But once I automated it, even with small amounts, it became surprisingly doable.

Here’s what goes into this 20%:

- Emergency fund contributions

- Retirement savings (401(k), IRA)

- Debt repayment beyond the minimums

- Investments (stocks, ETFs, crypto if you’re into that)

- Saving for big goals (a house, car, business, etc.)

The goal here is progress, not perfection.

If you can’t hit 20% right now, start with 5% or 10%, and increase it as your income grows or your expenses shrink.

Automate your savings and debt payments right after payday. When the money moves before you see it, you’ll never miss it, and your future self will thank you.

This 20% is what creates real financial breathing room. It’s how you move from “getting by” to “getting ahead.”

How To Apply the 50/30/20 Rule To Your Income

Okay, now that you know what the 50/30/20 budgeting rule is, let’s talk about how to actually use it.

The beauty of this method is that it works for any income level, you just adjust the numbers to fit your situation.

Here’s exactly how I apply it in my own budget:

Step 1: Know Your Take-Home Pay

Start with your after-tax income, the money that actually hits your bank account.

If you’re a freelancer or have variable income, take an average from the last few months.

Let’s say your monthly take-home pay is $3,000.

Step 2: Break It Down Using the 50/30/20 Budgeting Rule

Now, divide that income into each category:

|

Category |

Percentage |

Amount |

|---|---|---|

|

Needs |

50% |

$1,500 |

|

Wants |

30% |

$900 |

|

Savings/Debt |

20% |

$600 |

That’s your starting point.

Step 3: List Out Your Real Expenses

Go through your bills and spending for a month and see where everything fits.

- Rent, food, and transportation → Needs

- Dining out, Netflix, shopping → Wants

- Emergency fund, debt payments, investments → Savings/Debt

This helps you spot where you’re overspending and where to adjust.

Step 4: Automate and Track

Use tools like Mint, YNAB, or even a simple spreadsheet to keep tabs on your categories.

Automation is your best friend here, it turns good habits into default behavior.

Your first month won’t be perfect, and that’s okay. The goal is to build awareness and make gradual improvements. Over time, you’ll fine-tune your budget so it fits your lifestyle effortlessly.

Common Mistakes To Avoid

The 50/30/20 budgeting rule is simple, but that doesn’t mean it’s foolproof. When I first started using it, I made a few classic mistakes that nearly threw my budget off track.

If you want this method to work long-term, here are the biggest pitfalls to watch out for:

1. Treating “Wants” Like “Needs”

This one’s sneaky.

It’s easy to convince yourself that your favorite streaming services, daily lattes, or gym memberships are “needs.”

They’re not.

Be honest with yourself, if you can survive without it (even if you don’t want to), it belongs in the wants category.

Getting clear about this will instantly help you manage your money better.

2. Forgetting Irregular Expenses

Car repairs, birthdays, and holiday shopping have a way of showing up just when you feel like you’re doing great.

To stay ahead, set aside a little each month for those once-in-a-while expenses.

(Think of it as a mini “sinking fund.”)

3. Ignoring Income Changes

If your income goes up (or down), your 50/30/20 percentages should shift too.

It’s easy to forget this and end up spending more without realizing it.

Revisit your budget every few months or whenever your financial situation changes, promotions, side gigs, or new bills all count.

4. Forgetting the Goal Isn’t Perfection

When I first started budgeting, I’d get discouraged every time I went over in one category.

But here’s the truth, the goal isn’t to hit 50/30/20 perfectly every month.

The goal is awareness and balance.

If your “needs” hit 55% one month, adjust somewhere else next month. It’s about progress, not punishment.

5. Not Automating Your System

If you’re relying on willpower alone to save money, it’s going to be a struggle.

Automation makes it effortless, transfers happen before you can spend the money elsewhere.

Once I automated my savings and bill payments, my budget basically ran itself.

Think of the 50/30/20 budgeting rule as your financial GPS. It doesn’t matter if you make a few wrong turns, as long as you keep adjusting, you’ll always end up where you want to go.

How To Customize The Rule For Your Lifestyle

Here’s what I love most about the 50/30/20 budgeting rule: it’s flexible.

It’s not a rigid set of numbers you have to follow perfectly.

It’s a framework you can adjust to fit your goals, income, and situation.

When I first started using it, I had to tweak the percentages to match my reality, and that’s totally okay.

Here’s how you can make it your own 👇

1. Living in a High-Cost-of-Living Area

If you live somewhere where rent or housing eats up more than 50% of your paycheck, you’re not failing; you’re being realistic.

You might shift your split to something like:

60/20/20 (Needs/Wants/Savings)

or

70/20/10 temporarily until you can reduce costs or increase income.

The key is to still save something, even if it’s small. Consistency beats perfection every time.

2. Paying Off Debt Aggressively

If debt is your top priority, you can temporarily flip the ratios.

Try 50/20/30 – where 30% goes toward debt repayment and 20% covers your wants.

It might feel tough short-term, but the long-term relief is worth it.

3. Freelancers or Variable Income

When your income changes month to month, use percentages, not fixed amounts.

This keeps your budget adaptable.

Base your spending plan on your lowest monthly average income. That way, when you earn more, you can save the difference instead of overspending it.

4. Couples or Shared Finances

If you’re budgeting with a partner, treat the 50/30/20 budgeting rule as a team framework. Split expenses proportionally to income and agree on shared goals for savings and “wants.”

5. High Earners or Advanced Savers

Already have your essentials covered comfortably?

Consider a 40/20/40 split, where you increase your savings and investment portion.

At higher income levels, your focus shifts from survival to wealth building.

The magic isn’t in the exact percentages, it’s in the habit of dividing your income with purpose. Once you master that, you can fine-tune your ratios to match any stage of life.

Keep It Simple, Stay Consistent

If there’s one thing I’ve learned about money, it’s that complexity kills consistency.

I used to think managing money meant tracking every cent, checking spreadsheets daily, and constantly feeling guilty about spending.

But the 50/30/20 budgeting rule taught me something different: it’s not about perfection, it’s about balance.

When you give every dollar a clear purpose; some for needs, some for wants, and some for the future; everything starts to click. You stop guessing, stop stressing, and start feeling in control.

And the best part? You don’t have to overhaul your entire life to start.

Just take your next paycheck, divide it using the 50/30/20 framework, and give it a try for one month.

Then review, adjust, and repeat.

The best budget isn’t the one that looks perfect, it’s the one you’ll actually stick to.

So keep it simple. Stay consistent. Because when you manage your money intentionally, you’re not just balancing your budget, you’re building freedom.

Frequently Asked Questions (FAQ)

What is the 50/30/20 budgeting rule in simple terms?

The 50/30/20 budgeting rule is a simple budgeting method that divides your after-tax income into three parts:

50% for needs (bills, rent, groceries)

30% for wants (fun, entertainment, non-essentials)

20% for savings and debt repayment

It helps you manage your money without feeling restricted or overwhelmed.

Does the 50/30/20 budgeting rule actually work?

Yes, it works because it’s simple, flexible, and easy to maintain.

Unlike rigid budgets that track every penny, this method focuses on balance and awareness, not perfection. It helps you save consistently and spend intentionally.

How do I apply the 50/30/20 budgeting rule if my income is irregular?

If your income changes from month to month (like freelance or commission work), base your percentages on your average or lowest monthly income. When you earn more, save or invest the extra instead of increasing spending.

💬 Pro Tip:

Always prioritize your needs first, then distribute the rest between wants and savings.

How can I make the 50/30/20 budgeting rule work for couples?

The 50/30/20 budgeting rule is a great budgeting tool for couples. Treat the 50/30/20 budgeting rule as a team plan. Combine your after-tax income, cover shared “needs” first, then divide what’s left into joint “wants” and shared savings goals. Transparency and communication are key; agree on priorities and review them monthly.

Can I change the percentages if I have specific goals?

Absolutely! The 50/30/20 budgeting rule is just a framework. If you’re focused on paying off debt faster, you might do 50/20/30. If you’re trying to build wealth, try 40/30/30 or 40/20/40. The point is to give every dollar a job, not to follow a rigid formula.