The Pay Yourself First Strategy: How I Automated My Way to Real Savings

Are you scratching your head at the end of every month, wondering where your money went? I was…My paycheck came in, bills got paid, groceries happened, a few random Amazon boxes showed up, and somehow, by the time I checked my savings account, it was sitting at the exact same number it was 30 days ago. Sometimes less!

I decided to tackle this issue with the pay yourself first strategy. And, I wish someone had shown it to me years earlier.

I kept telling myself I would save “whatever was left over.” Spoiler alert: there was never anything left over!

Once I set up the pay yourself first strategy the right way, I no longer needed willpower at all. My savings just grew on their own while I was busy living my life.

If you are tired of feeling like you are working hard without anything to show for it, this system will turn things around for you. I am going to walk you through exactly what it is, why it works, and how to automate it in about 15 minutes.

What Is the Pay Yourself First Strategy?

The pay yourself first strategy is a budgeting method where you move money into savings the moment you get paid, before you pay any bills or spend on anything else. You automate a fixed transfer, usually 10 to 20 percent of your paycheck, from checking to a dedicated savings account, then live on what is left.

That is it. No fancy tracking. No envelopes. No hour-long Sunday money meetings.

It is sometimes called “reverse budgeting” because it flips the normal order. Instead of paying everyone else first and saving the scraps, you treat your savings goal like the most important bill you owe, and the one person you pay is future you. According to NerdWallet, this approach “treats savings like a recurring expense” rather than something you try to do after the fact.

Pay yourself first means savings is not optional and not last. It comes out first, automatically, before your brain even gets a chance to spend it.

Why The Pay Yourself First Strategy Actually Works

Most budgeting advice fails for one simple reason. It asks you to be disciplined every single day for the rest of your life. That is exhausting. It is also not how human brains work.

Pay yourself first works because it removes you from the equation. The money moves while you are sleeping. You never see it sitting in checking, so you never get a chance to spend it. Behavioral economists call this “friction reduction,” which is a fancy way of saying it is easier to do the right thing when the right thing happens on its own.

Here is what I noticed in my own life once I set it up:

- I stopped checking my savings balance because I knew it was growing automatically.

- I spent less on random stuff, because my checking account looked a little leaner and I naturally adjusted.

- I felt less guilty when I spent on fun things, because I knew my savings goal was already covered.

The Consumer Financial Protection Bureau has a whole section on building savings habits that work, and automation is at the top of the list. The theme is always the same. Make it automatic. Make it invisible. Let the system do the work.

How Much Should You Pay Yourself First?

The most common answer you will hear is 10-20% of your take-home pay. That range comes from financial planners, FDIC savings education, and most major banks, including PNC, which recommends automating “at least 10 percent” into savings before anything else.

But here is the honest version. The right amount is the amount you can actually stick to.

If 10 percent makes you panic, start with 1 percent. Yes, really. One percent of a $3,000 paycheck is $30. You will not notice it missing, and you will not sabotage the habit. Next month, bump it to 2 percent. Then 3. Within a year, you will be at 12 percent, and you will not have felt a single cent of it.

Here is a rough starter guide based on where you are:

The point is not to hit some perfect percentage on day one. It is to get the transfer running, on autopilot, so your savings can start growing today.

How to Set Up Pay Yourself First in 5 Steps

Here is the exact playbook I used, and it will take you about 15 minutes. No apps to download, no spreadsheets to build.

Step 1: Pick Your “Pay Yourself First” Account

Do not use the same bank as your checking account if you can help it. Use a separate high-yield savings account. This matters because money that sits in a different bank is harder to transfer on impulse, and a high-yield account pays you meaningfully more interest than the average 0.01% checking rate.

Step 2: Decide Your Percentage

Look at your last three paychecks. Pick a number that feels slightly uncomfortable but not scary. That is your starting percentage. Most people land somewhere between 5 and 10 percent for their first try.

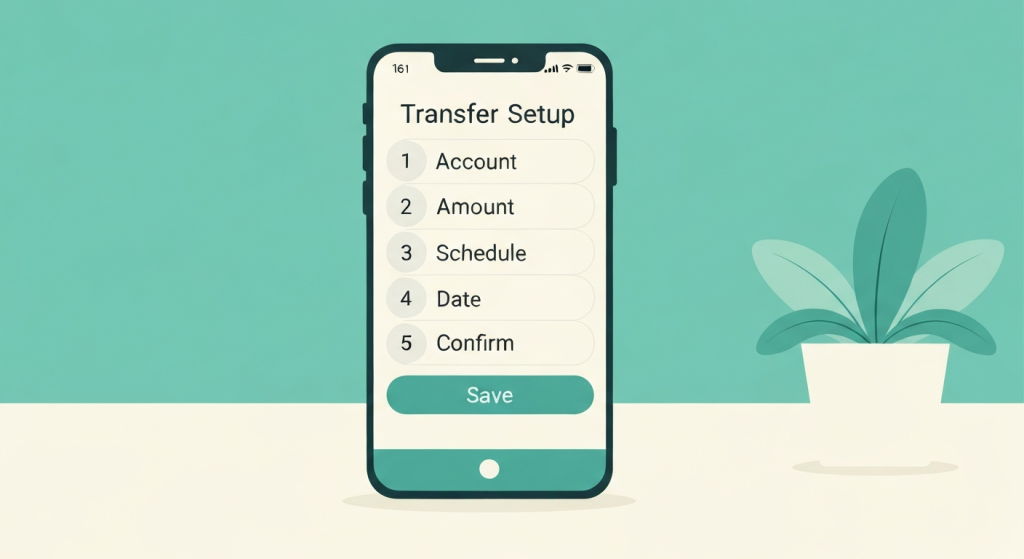

Step 3: Schedule the Automatic Transfer

Log in to your bank and set up a recurring transfer from checking to your new savings account. Time it for one or two days after payday so the deposit has cleared. If you get paid bi-weekly on Fridays, set the transfer for Saturday or Sunday.

Step 4: Ignore It for 30 Days

This step sounds silly but it is the most important one. For the first month, do not check the savings account. Do not mentally move money around. Just let it run. If you run short on anything, cover it from checking like normal and make a note of why.

Step 5: Review and Adjust

At the 30-day mark, check in. Did you survive the month without raiding savings? Great, consider bumping the percentage by 1 or 2 points. Did you struggle? Drop it by 1 point and try again. The goal is a number that runs on autopilot indefinitely.

That is the whole system. Five steps. One afternoon. A lifetime of savings that grows without you thinking about it.

Where Should Your “Pay Yourself First” Money Go?

Once you have the transfer running, the next question is where that money should actually land. Here is the priority order I recommend to almost everyone, and it lines up with what most major financial institutions suggest.

1. Emergency Fund First

If you do not have at least $1,000 set aside for emergencies, start there. This is your “the car broke down” money. It prevents a bad week from turning into credit card debt. I wrote a full guide on building an emergency fund from scratch if you want the step-by-step.

2. Sinking Funds for Known Expenses

Once your starter emergency fund is covered, split your pay-yourself-first money between a few sinking funds. These are small pots of money you are saving up for known expenses like holidays, car maintenance, or your annual insurance premium. Check out my breakdown of 20 common sinking fund categories to see what most people actually need.

3. Retirement Contributions

If your employer offers a 401(k) match, your pay-yourself-first money should capture at least that match. It is the closest thing to free money you will ever get.

4. Long-Term Wealth Building

Anything beyond the above can go into a taxable brokerage or Roth IRA, depending on your situation.

The key is that all of this happens automatically. You set the rules once and let the money flow into each bucket on its own.

Pay Yourself First vs. 50/30/20 vs. Zero-Based Budgeting

People often ask me how the pay yourself first strategy compares to other popular budgeting methods. Here is the short version.

Here is how I think about it. Pay yourself first is the foundation. You can layer 50/30/20 or zero-based budgeting on top if you want more structure. But if you only do one thing from this post, automating that first transfer will move the needle more than any fancy budgeting app ever will.

Common Mistakes People Make With Pay Yourself First

I have watched many people try this and fail, so I want you to avoid the exact traps I keep seeing.

Mistake 1: Saving into the Same Bank account

If your savings lives one tap away in the same app as your checking, you will raid it. Use a separate bank.

Mistake 2: Picking a Percentage That Is Too High

Going from saving nothing to saving 25 percent in one month is a recipe for blowing up the system. Start small, ramp up.

Mistake 3: Treating It Like a One-and-Done Task

Review your transfer every 6 months. Raises, new bills, and life changes mean your number should move too.

Mistake 4: Skipping the Automation

If you tell yourself, you will “manually transfer” it every Friday, you will forget, then skip it, then quit. Automate it or do not bother.

Mistake 5: Counting On Willpower

This is the biggest one. The whole point is that willpower is not involved. If your setup requires you to be disciplined, it is the wrong setup.

Tools That Make Pay Yourself First Easier

You do not need much to run this system. Here are the only tools I actually use:

- A High-yield Savings Account: Look for one with no monthly fees and an APY meaningfully above 4 percent. Some online banks currently pay more than 20 times what traditional banks offer on savings.

- Your Bank’s Built-in Recurring Transfer Feature: Every major bank has this. It is free.

- A Free budgeting App: If you want to track where your spending money is going after the transfer comes out, a simple app is plenty. You can see my list of savings automation tools for beginner-friendly picks.

That is really it. No paid software. No complicated spreadsheet. Just a bank, a transfer, and a little patience.

Final Thoughts

If I could go back and tell my younger self one thing about money, it would be this. Stop trying to save what is left over. There is never anything left over. Pay yourself first, automate it, and then get on with your life.

The pay yourself first strategy is not flashy. It will not go viral on TikTok. But it is the single most reliable way I know to turn “I wish I had savings” into “look at how much I have without even trying.”

Start with just one step today. Log into your bank, schedule a small recurring transfer for the day after your next payday, and let future you take it from there. That is how real savings get built.

Frequently Asked Questions

What does “pay yourself first” really mean?

Pay yourself first means you put money into your own savings account before you pay any bills or spend on anything else. It treats savings as a non-negotiable expense instead of something you do with leftover cash.

How much should I pay myself first from each paycheck?

A good starting target is 10 to 20 percent of your take-home pay. If that feels impossible, begin with 1 percent and raise it every month. The best amount is the one you can stick to without raiding the account.

Where should I put my “pay yourself first” money?

Priority order: a starter emergency fund, then sinking funds for known expenses, then any retirement match your employer offers, then long-term investing. All of it should be on autopilot.

What is the difference between pay yourself first and the 50/30/20 rule?

Pay yourself first only tracks one number, the amount you save. The 50/30/20 rule splits your income into three buckets (needs, wants, savings). You can use both together if you want more structure around your spending.

How long does it take to see results?

Most people see a real difference in 2 to 3 months. After a year of consistent automatic transfers, you will likely have more saved than in any previous year of trying to “save what is left over”.